Real Estate Physical Market Cycle Analysis – 5 Property Types – 54 Metropolitan Statistical Areas (MSAs).

It appears mid-term elections should not substantially change the pro-growth policies being pursued by the current administration, thus moderate economic growth should continue for the next few years. While US GDP growth has trended above the 2% average experienced since the great recession, slowing growth in Germany China and Japan may moderate US growth in the future. Full employment may push inflation and interest rates moderately over the next year. Demand growth continues in all the property types, with mild oversupply in apartments and hotels. We expect slowing supply growth due to labor shortages and higher construction costs.

Office occupancy increased 0.1% in 3Q18, and rents grew 0.5% for the quarter and 2.2% annually.

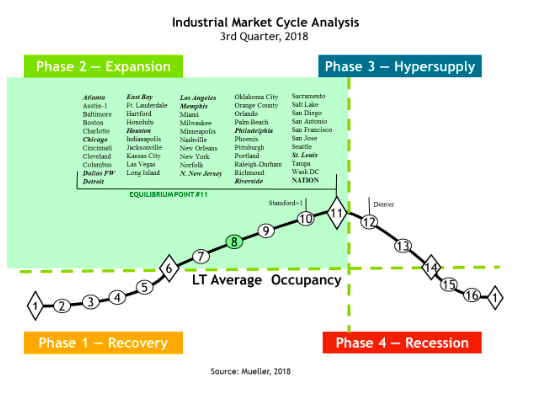

Industrial occupancy was flat in 3Q18, and rents grew 1.2% for the quarter and 5.9% annually.

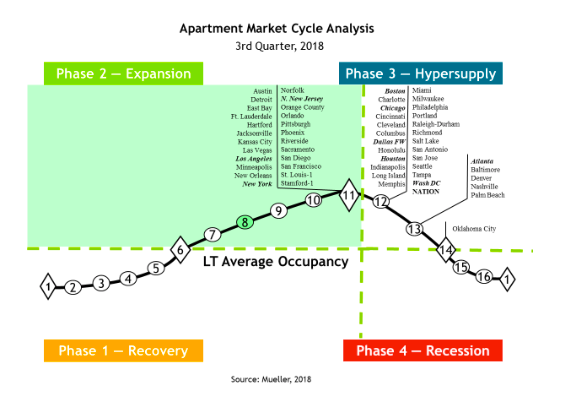

Apartment occupancy increased 0.1% in 3Q18, and rents grew 0.2% for the quarter and 3.2% annually.

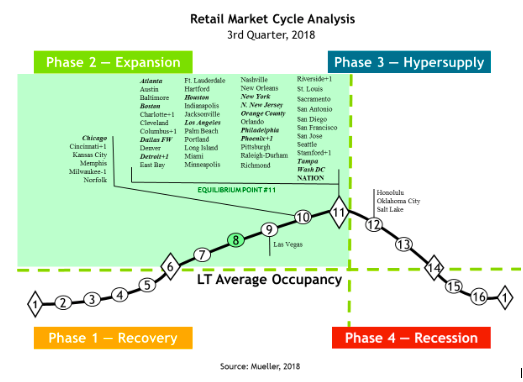

Retail occupancy was flat in 3Q18, and rents grew 0.2% for the quarter and 1.6% annually.

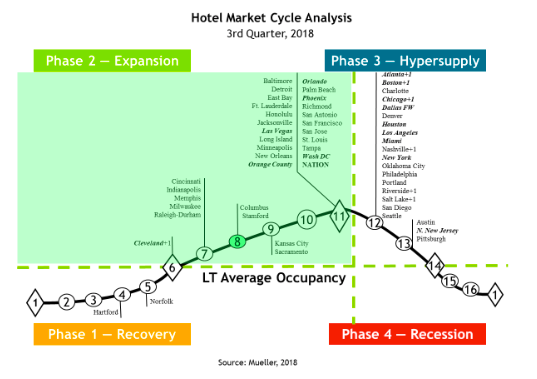

Hotel occupancy declined 0.2% in 3Q18, and room rates grew 0.8% for the quarter and 3.3% annually.

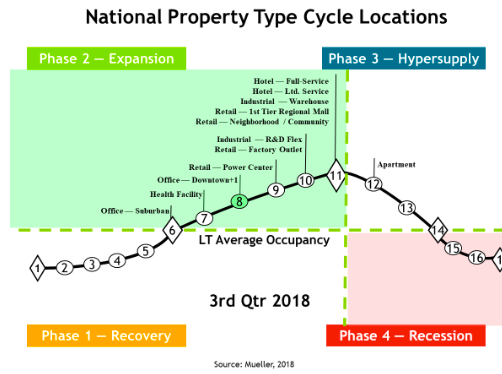

The National Property Type Cycle Locations graph shows relative positions of the sub-property types.

Glenn R. Mueller, Ph.D. – Professor, Burns School of Real Estate & Construction Management – glenn.mueller@du.edu University of Denver – https://daniels.du.edu/burns-school.

The cycle monitor analyzes occupancy movements in five property types in 54 MSAs. Market cycle analysis should enhance investment-decision capabilities for investors and operators. The five property type cycle charts summarize almost 300 individual models that analyze occupancy levels and rental growth rates to provide the foundation for long-term investment success. Commercial real estate markets are cyclical due to the lagged relationship between demand and supply for physical space. The long-term occupancy average is different for each market and each property type. Long-term occupancy average is a key factor in determining rental growth rates — a key factor that affects commercial real estate income and thus returns.

Office

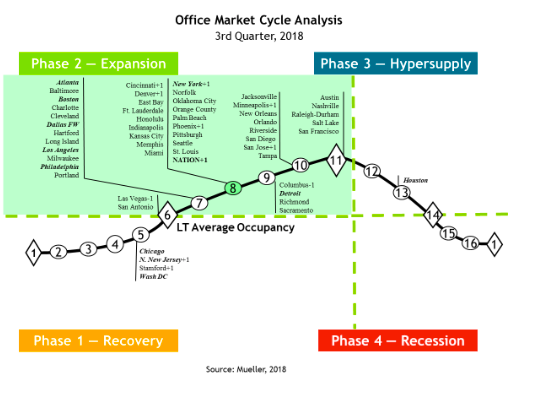

The national office market occupancy level increased 0.1% in 3Q18 and was up 0.1% year-over-year. Office employment growth was constrained by full employment, as firms found it difficult to hire from a smaller hiring pool. New supply is moderate, as higher construction and financing costs are creating better rationalization. Short term rentals like WeWorks is leading new demand for space as small start-ups need the growth flexibility and larger firms realize that the tax code now favors short terms rentals that do not have to be accounted for as debt on their balance sheets like long term leases. National average occupancy has moved to point #8 (the cost feasible rent level) so expect more new construction. All but five markets are now in the growth phase of the occupancy cycle! Average national rents increased 0.5% in 3Q18 and produced a 2.2% increase year-over-year.

Note: The 11-largest office markets make up 50% of the total square footage of office space we monitor. Thus, the 11-largest office markets are in bold italic type to help distinguish how the weighted national average is affected.

Markets that have moved since the previous quarter are now shown with a + or – symbol next to the market name and the number of positions the market has moved is also shown, i.e., +1, +2 or -1, -2. Markets do not always go through smooth forward-cycle movements and can regress or move backward in their cycle position when occupancy levels reverse their usual direction. This can happen when the marginal rate of change in demand increases (or declines) faster than originally estimated or if supply growth is stronger (or weaker) than originally estimated.

Industrial occupancies were flat in 3Q18 and increased 0.2% year-over-year. Remember that peak occupancy is also economic equilibrium, where demand and supply are BOTH growing at the same balanced rate. In a perfect world, markets would be at equilibrium point #11 at all times. Retailers building out their internet delivery systems continue to be the major driver of industrial demand. Closer in warehouse for same day delivery is also an additional demand driver. There is also a demand boost when recreational marijuana is legalized in any state, and now with Massachusetts being the first eastern state, more should follow. Industrial national average rents increased 1.2% in 3Q18 and increased 5.9% year-over-year.

Note: The 12-largest industrial markets make up 50% of the total square footage of industrial space we monitor. Thus, the 12-largest industrial markets are in bold italic type to help distinguish how the weighted national average is affected.

Markets that have moved since the previous quarter are now shown with a + or – symbol next to the market name and the number of positions the market has moved is also shown, i.e., +1, +2 or -1, -2. Markets do not always go through smooth forward-cycle movements and can regress or move backward in their cycle position when occupancy levels reverse their usual direction. This can happen when the marginal rate of change in demand increases (or declines) faster than originally estimated or if supply growth is stronger (or weaker) than originally estimated.

Apartment

The national apartment occupancy average improved 0.1% in 3Q18 and improved 0.4% year-over-year. Moderate demand growth continues and increasing interest rates are helping to slow the number of renters leaving to buy a house. Increasing construction costs and increasing interest rates are finally starting to moderate the over-supply that has happened over the past five years. If supply moderation continues, it is possible that many apartment markets could move back into the growth phase. Average national apartment rent growth was up 0.2% in 3Q18 and national average rents increased 3.2% year-over-year.

Note: The 10-largest apartment markets make up 50% of the total square footage of multifamily space we monitor. Thus, the 10-largest apartment markets are in bold italic type to help distinguish how the weighted national average is affected.

Markets that have moved since the previous quarter are now shown with a + or – symbol next to the market name and the number of positions the market has moved is also shown, i.e., +1, +2 or -1, -2. Markets do not always go through smooth forward-cycle movements and can regress or move backward in their cycle position when occupancy levels reverse their usual direction. This can happen when the marginal rate of change in demand increases (or declines) faster than originally estimated or if supply growth is stronger (or weaker) than originally estimated.

Retail

Retail occupancies were again flat in 3Q18 and were up 0.2% year-over-year. All but ten markets are at peak occupancy. Remember that peak occupancy is also economic equilibrium, where demand and supply are BOTH growing at the same balanced rate. New experienced based formats continue to take over vacated space from traditional retailers going out of business. Many mall owners are now working toward creating mini-cities with apartments, offices and more food and entertainment options to both fill existing space and create space demand. National average retail rents increased 0.2% in 3Q18 and increased 1.6% year-over-year.

Note: The 14-largest retail markets make up 50% of the total square footage of retail space we monitor. Thus, the 14-largest retail markets are in bold italic type to help distinguish how the weighted national average is affected.

Markets that have moved since the previous quarter are now shown with a + or – symbol next to the market name and the number of positions the market has moved is also shown, i.e., +1, +2 or -1, -2. Markets do not always go through smooth forward-cycle movements and can regress or move backward in their cycle position when occupancy levels reverse their usual direction. This can happen when the marginal rate of change in demand increases (or declines) faster than originally estimated or if supply growth is stronger (or weaker) than originally estimated.

Hotel

Hotel occupancies were down -0.2% in 3Q18 and flat year-over-year. Room demand remains strong from both business and leisure travel with the higher current economic expansion. New construction continues to push supply in a number of markets with six markets experiencing lower occupancy, thus moving them into the hyper-supply phase of the cycle this quarter. Over supply is the key risk for hotels at this time. Many new niche and unique format hotels continue to emerge and the Air-B&B expansion continues as well. The Marriott – Starwood merger integration has taken longer than expected but improved their loyalty program attraction by expanding stay options. We expect to see them acquire and build more hotels going forward. The national average hotel room rate increased 0.8% in 3Q18 and increased 3.3% year-over-year.

Market Cycle Analysis — Explanation

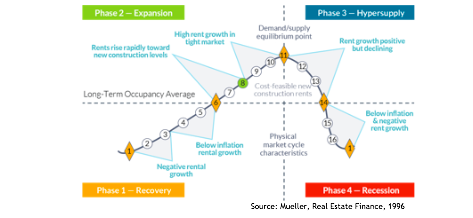

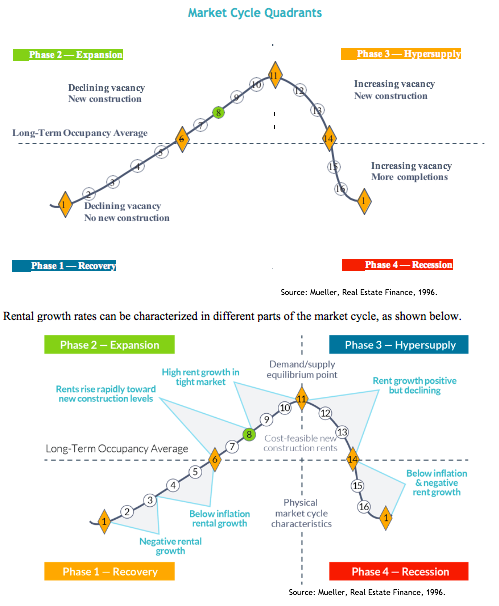

Supply and demand interaction is important to understand. Starting in Recovery Phase I at the bottom of a cycle (see chart below), the marketplace is in a state of oversupply from either previous new construction or negative demand growth. At this bottom point, occupancy is at its trough. Typically, the market bottom occurs when the excess construction from the previous cycle stops. As the cycle bottom is passed, demand growth begins to slowly absorb the existing oversupply and supply growth is nonexistent or very low. As excess space is absorbed, vacancy rates fall, allowing rental rates in the market to stabilize and even begin to increase. As this recovery phase continues, positive expectations about the market allow landlords to increase rents at a slow pace (typically at or below inflation). Eventually, each local market reaches its long-term occupancy average, whereby rental growth is equal to inflation.

In Expansion Phase II, demand growth continues at increasing levels, creating a need for additional space. As vacancy rates fall below the long-term occupancy average, signaling that supply is tightening in the marketplace, rents begin to rise rapidly until they reach a cost-feasible level that allows new construction to commence. In this period of tight supply, rapid rental growth can be experienced, which some observers call “rent spikes.” (Some developers may also begin speculative construction in anticipation of cost-feasible rents if they are able to obtain financing). Once cost-feasible rents are achieved in the marketplace, demand growth is still ahead of supply growth — a lag in providing new space due to the time to construct. Long expansionary periods are possible and many historical real estate cycles show that the overall up-cycle is a slow, long-term uphill climb. As long as demand growth rates are higher than supply growth rates, vacancy rates will continue to fall. The cycle peak point is where demand and supply are growing at the same rate or equilibrium. Before equilibrium, demand grows faster than supply; after equilibrium, supply grows faster than demand.

Hypersupply Phase III of the real estate cycle commences after the peak / equilibrium point #11 — where demand growth equals supply growth. Most real estate participants do not recognize this peak / equilibrium’s passing, as occupancy rates are at their highest and well above long-term averages, a strong and tight market. During Phase III, supply growth is higher than demand growth (hypersupply), causing vacancy rates to rise back toward the long-term occupancy average. While there is no painful oversupply during this period, new supply completions compete for tenants in the marketplace. As more space is delivered to the market, rental growth slows. Eventually, market participants realize that the market has turned down and commitments to new construction should slow or stop. If new supply grows faster than demand once the long-term occupancy average is passed, the market falls into Phase IV.

Recession Phase IV begins as the market moves past the long-term occupancy average with high supply growth and low or negative demand growth. The extent of the market down-cycle will be determined by the difference (excess) between the market supply growth and demand growth. Massive oversupply, coupled with negative demand growth (that started when the market passed through long-term occupancy average in 1984), sent most U.S. office markets into the largest down-cycle ever experienced. During Phase IV, landlords realize that they will quickly lose market share if their rental rates are not competitive. As a result, they then lower rents to capture tenants, even if only to cover their buildings’ fixed expenses. Market liquidity is also low or nonexistent in this phase, as the bid–ask spread in property prices is too wide. The cycle eventually reaches bottom as new construction and completions cease, or as demand growth turns up and begins to grow at rates higher than that of new supply added to the marketplace.