Industrial and logistics (I&L) REITs in the Pacific Rim played an added-value and strategic role in multi-asset portfolios, according to our new analysis published in the Journal of Property Investment & Finance.

E-commerce is driving an increased level of industrial and logistics property space demands. This trend has been amplified by the covid-19 pandemic. To accommodate increasing I&L property demand, I&L REITs have recently enhanced their property portfolios, often replacing the traditional industrial properties with logistic properties to gain strategic exposure to recent e-commerce trends.

How does e-commerce drive I&L property space demand?

An omnichannel retail platform strategy and a dynamic supply chain ecosystem with high digital technologies have been employed by e-retailers (e.g. Amazon, eBay, Alibaba) to meet the rapid growth of e-commerce activities.

These high-tech advances, including the use of smart devices (e.g. laptops, tablets, smartphones, smart TV) and social media platforms (e.g. Facebook, Twitter, Instagram, YouTube), have driven online shoppers to demand faster and more frequent delivery (just-in-time aka JIT procedures). In doing so, increasing I&L property space demands (e.g. third-party logistics aka 3PL, food and beverage, building supplies, consumer goods) are expected. To accommodate increasing I&L property space demand, logistics properties have taken on increased levels in I&L REIT portfolios (e.g. Goodman, Ascendas REIT), replacing the traditional style of industrial properties. For example, Goodman group increased the logistics property exposure in its property portfolio from 78% in 2007 to 94% in 2018.

Key I&L REIT players

Four of the top five global I&L REITs are in the Pacific Rim region. In particular, the region constituted 89.0% of the total global market capitalisation of I&L REITs in 2018, including the US (US$79.0bn), Japan (US$14.7bn), Australia (US$14.9bn) and Singapore (US$15.9bn). Strong growth of I&L REITs has been evident in the Pacific Rim region. The size of I&L REITs in the region increased from US$34.8bn in July 2011 to US$124.5bn in December 2018, with an increase of 3.6 times over this period.

Players of Pacific Rim-based I&L REITs are Prologis (US; no. 1 in the region as of December 2018; US$38.0bn), Goodman (Australia; no. 2; US$13.6bn), Duke Realty (US; no. 3; US$9.3bn), Liberty property trust (US; no. 4; US$6.3bn), Ascendas REIT (Singapore; no. 5; US$5.9bn), Nippon Prologis REIT (Japan; no. 6; US$4.6bn), GLP J-REIT (Japan; no. 8; US$3.9bn), Mapletree logistics trust (Singapore; no. 11; US$3.7bn), Japan logistics (Japan; no. 16; US$1.9bn) and ESR-REIT (Singapore; no. 19; US$1.2bn).

Investment performance of I&L REITs

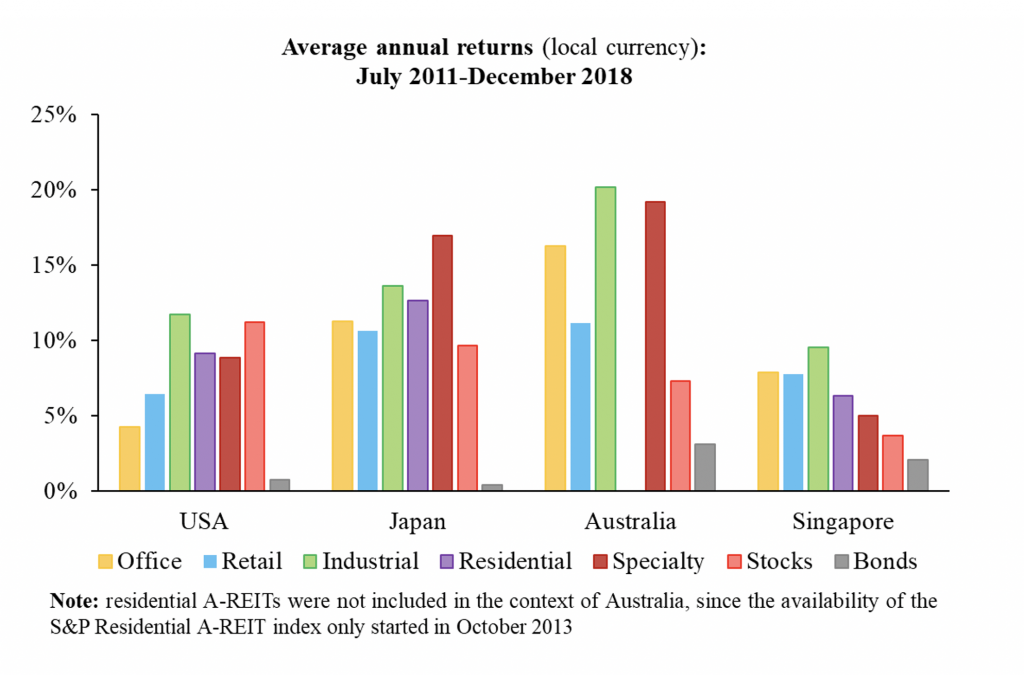

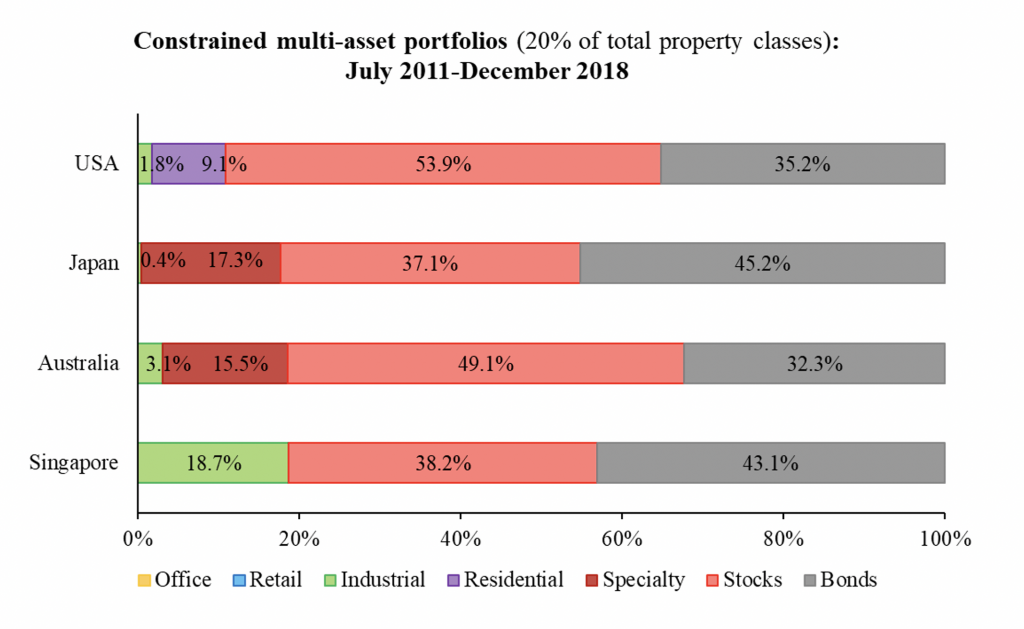

I&L REITs in the Pacific Rim region delivered superior average annual returns compared with other property types of REITs, stocks and bonds in the US, Japan, Australia and Singapore. Further, I&L REITs enhanced portfolio returns and generally offered stronger diversification benefits with both stocks and bonds than other property types of REITs in each case.

Importantly, I&L REITs played a more significant role than other property types of REITs in a multi-asset portfolio across the US, Japan, Australia and Singapore. These findings confirm the added-value role of Pacific Rim-based I&L REITs in multi-asset portfolios in these four markets, with strong diversification benefits for international property investors seeking portfolio diversification in the Pacific Rim region.

What next?

The research findings have several significant listed property investment implications:

1. Property investors are advised to consider including Pacific Rim-based I&L REITs within their multi-asset portfolios, given the strong investment performance of I&L REITs in the Pacific Rim region.

2. REIT investment advisers should consider recommending I&L REITs to their clients who intend to develop a new REIT portfolio in the Pacific Rim region, capturing the growth dynamics of the Pacific Rim and in logistics property space demand.

3. To gain strategic exposure to e-commerce trends in the Pacific Rim region, international property investors should consider investing in Pacific Rim-based I&L REITs, which have rotated the traditional industrial property structures to logistics property formats in the post-GFC context.

4. Property investors should acknowledge the differential I&L REIT portfolio allocations in each of the four markets. This could be attributed to the different growth speed of trade in commercial services in different markets.

This article is a summary from Lin, Y.-C., Lee, C.L. and Newell, G. (2020), “The Added-Value Role of Industrial and Logistics REITs in the Pacific Rim Region” in the Journal of Property Investment & Finance. The full article is available here.